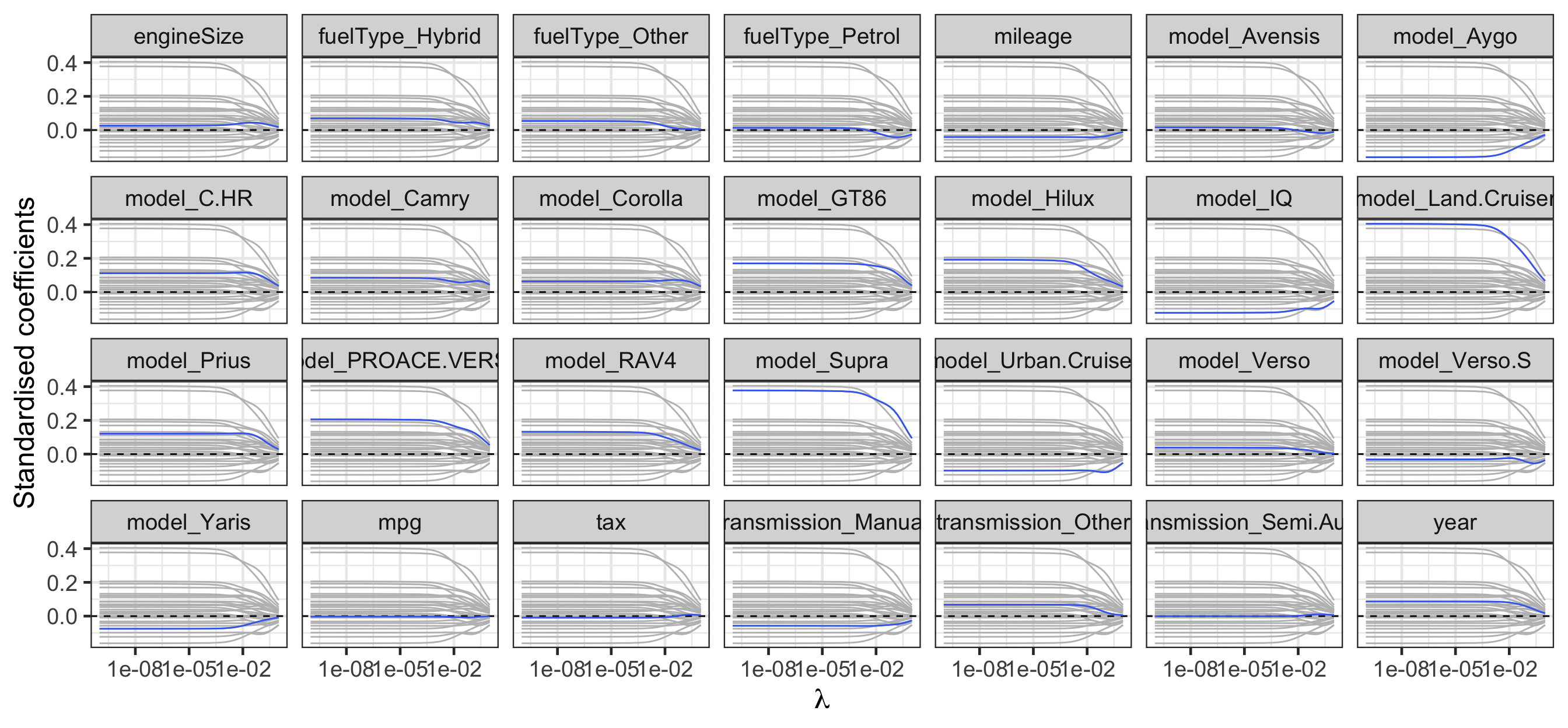

Regularisation path for ridge regression

Code

library(broom) # for tidy

fit_ridge %>%

tidy(return_zeros = TRUE) %>%

filter(term != "(Intercept)") %>%

ggplot(aes(lambda, estimate)) +

geom_line(data = ~rename(., term2 = term),

aes(group = term2),

color = "grey") +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_line(color = "royalblue2") +

facet_wrap(~term, nrow = 4) +

labs(x = latex2exp::TeX("\\lambda"),

y = "Standardised coefficients") +

scale_x_log10()

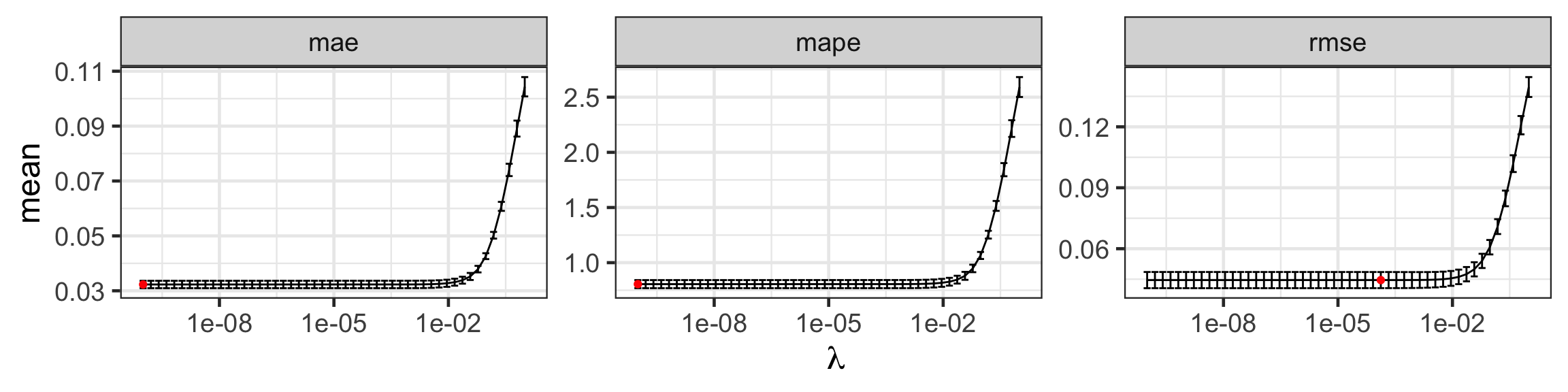

Selecting the tuning parameter for ridge regression

Code

toyota_tuning_ridge_min <- toyota_tuning_ridge %>%

group_by(.metric) %>%

filter(mean == min(mean))

toyota_tuning_ridge %>%

ggplot(aes(lambda, mean)) +

geom_errorbar(aes(ymin = mean - se,

ymax = mean + se)) +

geom_line() +

geom_point(data = toyota_tuning_ridge_min,

color = 'red') +

facet_wrap(~.metric, scales = "free") +

scale_x_log10(name = latex2exp::TeX("\\lambda"))

| Metric | \(\lambda\) | Mean | Std. Error |

|---|---|---|---|

| rmse | 0.0001326 | 0.0445490 | 0.0039625 |

| mae | 0.0000000 | 0.0322999 | 0.0013496 |

| mape | 0.0000000 | 0.8054924 | 0.0367295 |

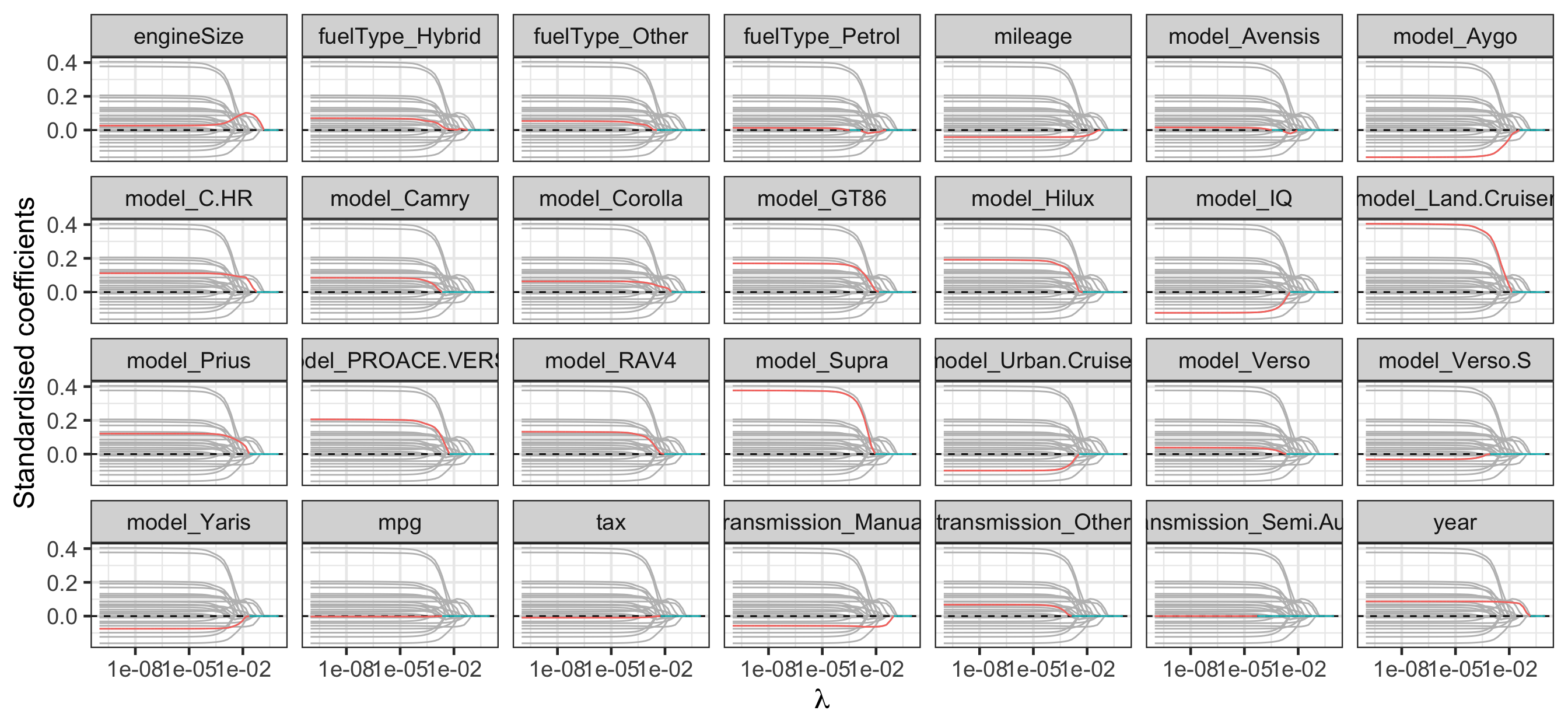

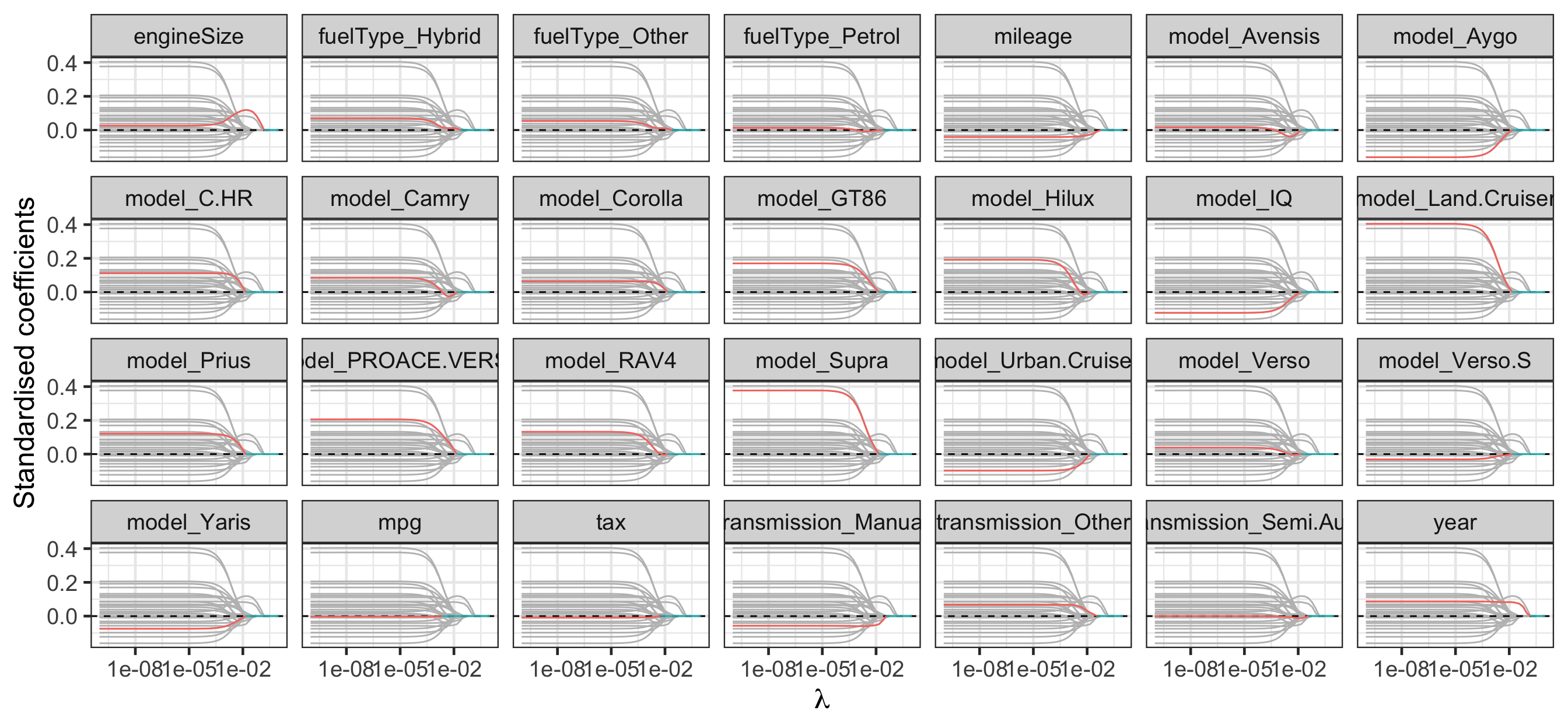

Regularisation path for lasso

Code

library(broom) # for tidy

est_lasso <- fit_lasso %>%

tidy(return_zeros = TRUE)

est_lasso %>%

filter(term != "(Intercept)") %>%

mutate(zero = estimate == 0) %>%

ggplot(aes(lambda, estimate)) +

geom_line(data = ~rename(., term2 = term),

aes(group = term2),

color = "grey") +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_line(aes(color = zero, group = term)) +

facet_wrap(~term, nrow = 4) +

labs(x = latex2exp::TeX("\\lambda"),

y = "Standardised coefficients") +

guides(color = "none") +

scale_x_log10()

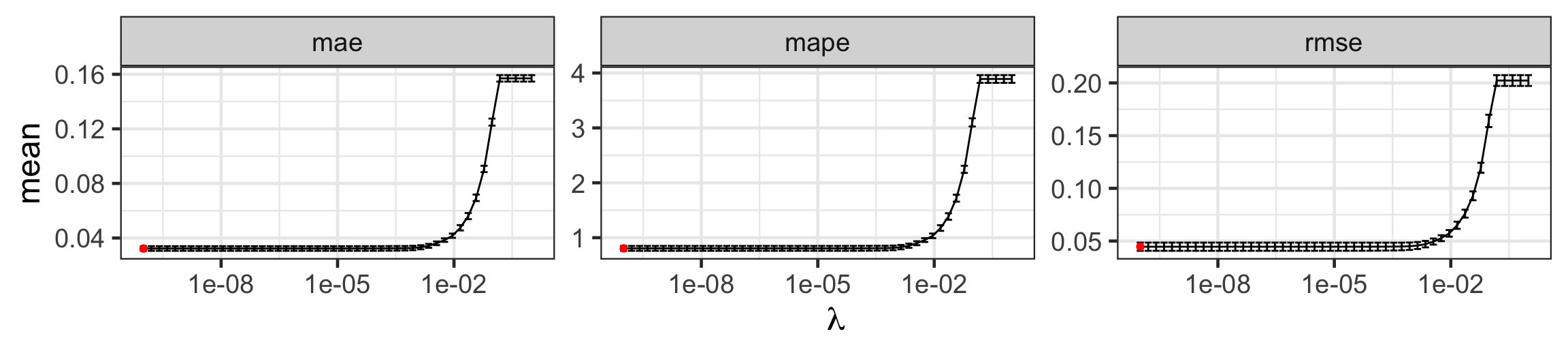

Selecting the tuning parameter \(\lambda\) for lasso

Code

toyota_tuning_lasso <- cv_glmnet_to_toyota(alpha = 1)

toyota_tuning_lasso_min <- toyota_tuning_lasso %>%

group_by(.metric) %>%

filter(mean == min(mean))

toyota_tuning_lasso %>%

ggplot(aes(lambda, mean)) +

geom_errorbar(aes(ymin = mean - se,

ymax = mean + se)) +

geom_line() +

geom_point(data = toyota_tuning_lasso_min,

color = 'red') +

facet_wrap(~.metric, scales = "free") +

scale_x_log10(name = latex2exp::TeX("\\lambda"))

| Metric | \(\lambda\) | Mean | Std. Error |

|---|---|---|---|

| mae | 0 | 0.0323048 | 0.0017061 |

| mape | 0 | 0.8057043 | 0.0447169 |

| rmse | 0 | 0.0446230 | 0.0039084 |

Regularisation path for group lasso

Code

est_glasso <- fit_glasso %>%

broom:::tidy.glmnet(return_zeros = TRUE)

est_glasso %>%

mutate(zero = estimate == 0) %>%

filter(term != "(Intercept)") %>%

ggplot(aes(lambda, estimate)) +

geom_line(data = ~rename(., term2 = term),

aes(group = term2),

color = "grey") +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_line(aes(color = zero, group = term)) +

facet_wrap(~term, nrow = 4) +

labs(x = latex2exp::TeX("\\lambda"),

y = "Standardised coefficients") +

scale_x_log10() +

guides(color = "none")

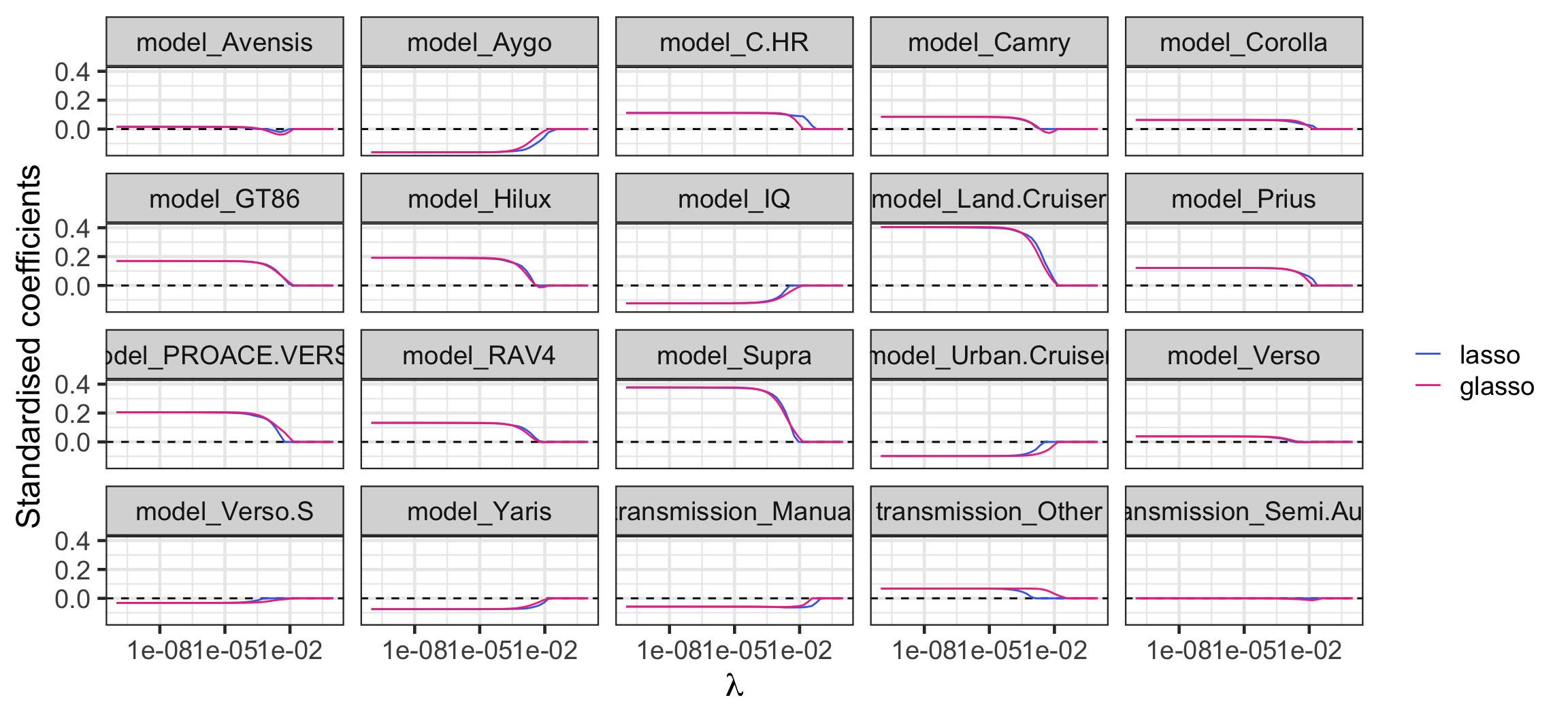

Regularisation path: lasso vs group lasso

scroll

Code

bind_rows(mutate(est_lasso, type = "lasso"),

mutate(est_glasso, type = "glasso")) %>%

mutate(type = fct_inorder(type),

zero = estimate == 0) %>%

filter(str_detect(term, "^(model_|transmission_)")) %>%

ggplot(aes(lambda, estimate)) +

geom_hline(yintercept = 0, linetype = "dashed") +

geom_line(aes(group = interaction(term, type), color = type)) +

facet_wrap(~term) +

labs(x = latex2exp::TeX("\\lambda"),

y = "Standardised coefficients") +

scale_x_log10() +

scale_color_manual("", values = c("royalblue2", "violetred2"))

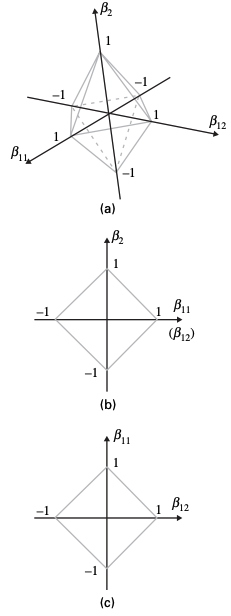

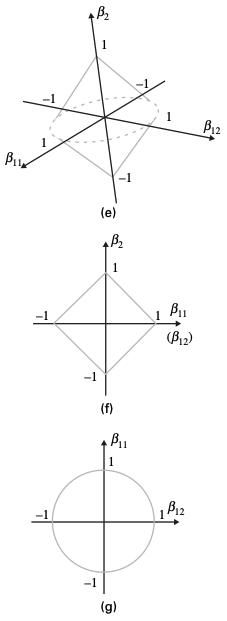

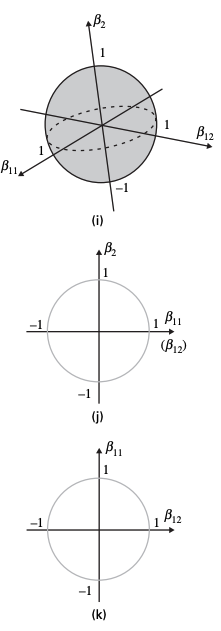

Visualising the constraints

Lasso

Group lasso

Ridge regression

Takeaways

- Shrinkage methods are a powerful variable selection approach for regression by shrinking the coefficients predictors towards zero.

- You can use cross-validation to calibrate these methods for prediction.